Hey! Welcome to Marginal Futility. Here, I share interesting things I come across, especially related to business, finance and tech. You can find my previous posts here.

You can subscribe below if you wish to receive updates directly in your mailbox. No spam, ever! :) You can also follow me on Twitter here.

On to today’s post…

«Finance»

How employee compensation schemes masquerade as buybacks

Having a “finance” section in a newsletter is, in my opinion, a readership limiting move; and then using that section to talk about something dry like “buybacks” is even worse.

But bear with me - this post is based on a genuinely eye-opening article By Ben Hunt (Epsilon Theory) that I recently read. Buybacks are one of those things that you don’t think twice about because they seem quite straightforward; and one day you realize they aren’t.

First, a quick 1 minute intro to stock buybacks.

Let’s say a company has left over cash - after funding current operations, after doing whatever it has to do to grow further and after paying its other obligations like interest. Now, it can return the money to its shareholders or it can keep it with itself, preparing a war chest of sorts to do something in future. Lets say it decides to return the money because it feels it cannot put it to much productive use within the business. Keep in mind - this is money that “belongs” to the shareholders. Now how to return money?

Two ways. First - you pay your shareholders in cash (called Dividends). Pretty straightforward.

Second - you tell your shareholders - “Look, I am willing to buy shares worth XX dollars from you”. These are called stock buybacks.

What is the benefit of this? Yes, the shareholders cashing out get to sell their shares at typically a slight premium to the traded price of the share. But that’s not it. The crucial benefit of buybacks is that the shareholders who continue to stay on benefit from an increased share of the pie. Per share value is essentially the company value divided by no. of shares, and reducing the denominator means the remaining shares are worth more. This is the true ‘return of money’ - you ‘return’ money to your continuing shareholders by making their shares more valuable.

Given tax laws are typically more favorable for buybacks, they are a very credible and often preferred alternative to cash dividends.

Note the important part - Share count MUST reduce so that the shares remaining with the continuing shareholders become more valuable. Share count MUST reduce if you are truly returning money to your shareholders.

…

Lets look at the buyback numbers of Meta and Apple over the past 10 years.

1️⃣ Meta spent USD 96 billion in stock buybacks over the last 10 years; and Apple spent 554 billion.

This is obviously looking great; and a testament to the high cash generating engines these companies have built.

But wait. Remember that during this period, they also rewarded their employees through share based compensation (ESOPs/ Restricted Share Units) - Quite an acceptable practice; and frankly, the right thing to do to align employee interests well.

While the buybacks reduced share counts; share based compensation (SBC) to employees increases share count.

What’s the net impact?

2️⃣ Despite the humongous amount spent on buybacks, Meta’s share count *increased* 12% over the past 10 years. Apple, on the other hand, managed to reduce its share count by around 38%.

Hmm. So buybacks are supposed to benefit continuing shareholders by reducing the effective number of shares; making each share more valuable. But it seems that Meta has not managed to do this through its buybacks.

Because there was a force working in exactly opposite direction - SBC offered to employees.

…

Now,, lets add some more details to the above table.

3️⃣ The ratio of new shares issued to employees divided by the shares bought back by the company is the buyback sterilization percentage.

This denotes the percentage of money spent on buybacks which actually went on to sterilize (offset) the dilutive new shares issued to employees. While numerically capped at 100% (denoting all buyback dollars went towards offsetting new shares); in Meta’s case, its quite clear that the buybacks don’t even fully offset the new shares - hence, the increase in share count over the period.

Multiply the buyback sterilization % with total amount spent on buybacks to get the absolute amount of money which went on to offset dilutive impact of stock based compensation.

4️⃣ Free Cash Flow (FCF) is the money left for debt holders and equity shareholders of the company. It’s the cash that’s left over after the company has spent whatever it must spend to maintain and grow its operations.

Meta spent 77% of its FCF over a decade to monetize/ offset the stock based compensation awarded to its employees (over and above the cash salaries).

In contrast, Apple spent only 12% - and remember, it reduced the overall share count by 38% during this period.

….

The above table is just one side of the story. It showed the buyback money effectively spent on offsetting share based comp to employees.

The next table shows the money “truly returned” to the continuing shareholders.

1️⃣ The effective benefit of buybacks in case of Meta is predictably lower; due to the high sterilization %

Note: Meta does not give dividends.

From their 10-Q,

We do not intend to pay cash dividends for the foreseeable future.

We have never declared or paid cash dividends on our capital stock. We currently intend to retain any future earnings to finance the operation and expansion of our business and fund our share repurchase program, and we do not expect to declare or pay any cash dividends in the foreseeable future.

Total capital “effectively” returned to continuing shareholders (net of offsetting impact of SBC) is 0% of FCF for Meta; and 92% for Apple.

0% of FCF (money actually belonging to shareholders after debt commitments) actually effectively spent to benefit continuing shareholders!

Meanwhile, Apple has effectively given out more than 600bn in buybacks and dividends over a 10 year period!

………

Now, as I said before, rewarding employees via share based compensation is needed and the right thing to do.

But doing so as such a scale; wherein massive buybacks have to be conducted to only to offset the dilutive impact of SBC, does not seem right.

Buybacks are often touted as returning cash to shareholders; and boosting EPS of remaining shares through reduced share count. This did not happen here

A buyback is a capital allocation decision - the management is effectively saying that buying back stock of the company is the best use of leftover funds. What follows obviously from here is that a management should do a buyback when it feels that the share price is very undervalued as compared to intrinsic value. But if buybacks are a ‘necessity’ to offset the dilutive impact of share based compensation to employees and management, how does the management even make sure they are buying back stock at the right times? They could very well be buying back shares at valuations dramatically higher than intrinsic value. This is capital misallocation, no matter which way you look at it.

P.S. Avg. buyback price of $254 over 10 years vs current market price of $114 for Meta

…

So here’s the bottom line. If the company did not do buybacks at such a scale, the dilution impact of all ESOPs would have been humongous. In effect, the ESOPs necessitated the buybacks. So it it really returning money to the continuing shareholders? Or is it an employee compensation scheme masquerading as a buyback - a transfer of wealth from shareholders to employees while extolling the virtues of buybacks?

Ofcourse, Meta is not the only one guilty of this. A buyback analysis of Twitter, Texas Instruments, JP Morgan and several other companies would paint the same picture.

One of the first things we were taught in accounting and financial analysis was valuing Substance over form. I used to have a very favourable opinion of buybacks, but from here on, I will always be evaluating whether buybacks are being done for the shareholders or just for the employees.

«Business»

Several of the success stories we have seen in the Indian startup ecosystem are from the Business to Consumer (B2C) space - Flipkart, Swiggy, Ola etc. These are companies which deal with the end customer.

However, before the product/ service reaches or is consumed by the final consumer, there are several layers in between; where several business to business (B2B) transactions happen.

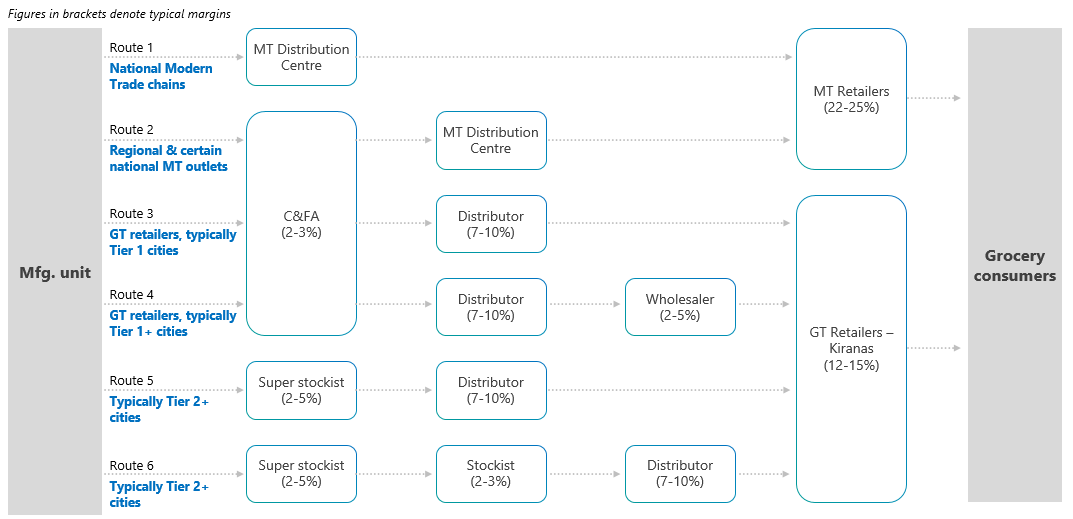

B2B commerce in India is highly fragmented and complex, comprising several layers of intermediaries and wholesalers, who connect manufacturers/ brands with a vast ecosystem of mom-and-pop retail stores.

As an illustration, this is how a standard, organized value chain for grocery looks like.

Source: Redseer

As we start moving towards unorganized and non-distributed value chains; there are even more intermediaries involved; and hence, a much higher level of complexity.

A fragmented and layered supply chain creates several challenges for both sides of the value chain — brands & manufacturers and retailers.

e-B2B entails the application of e-commerce in the B2B trade. e-B2B players take in orders from retailers online (website or app) and deliver the merchandise to the retail outlet, very similar to the services offered by unorganised distributors/ wholesalers. Faster and timely deliveries, attractive prices, and a wider assortment across brands and categories are the key areas where e-B2B differentiates itself from unorganised vendors.

While e-commerce adoption in B2C has grown in the last decade, eB2B is still in the nascent stages. Appx size in FY22 would be around ~USD 4 bn; and has less than 1% share of overall pie.

Some players in the eB2B space have taken a multi-category (horizontal) approach - for eg. Udaan, Flipkart Wholesale, Reliance Retail (JioMart Kirana).

However, several others are building a vertical platform focused on a single category. Following is an illustrative list of vertical B2B marketplaces.

Source: Alter VC

I recently came across an interesting podcast series on B2B marketplaces by Matrix Partners. One of the things discussed was a preference towards vertical marketplaces from an investing standpoint.

Here’s what Sudipto Sannigrahi, Principal at Matrix Partners, says about this.

If you look at B2C, right, what does a marketplace do?

They essentially acquire a customer by probably selling electronics at a very competitive price and then over a period of time make money by selling clothes, private labels, by selling books, by selling a lot of other products which have higher gross margin and you can make money from them.

So B2C is essentially how do you acquire a customer and then amortize that cap by selling a lot of other products where you can make money…

Now let’s take B2B. You sell electronics to a customer, will that customer ever buy fashion from you?

So the guy who sells electronics, the retailer who sells electronics does not sell fashion. So you cannot essentially acquire a customer and sell multiple different products to them. So the customer set across verticals is different

…the kind of factory and the form factor of factory and the geographical disposition of the factory is very different. So customers are different, the sellers are different. On top of that your logistics and supply chain is completely different….the storage, first mile, last mile is completely different. On top of that credit, payment, underwriting, that is again very different in each supply chain...Which means if you want to do horizontal you’re not building one company you’re building multiple companies.

A vertical shift allows for optimization across several metrics:

Higher assortment. Focusing on one specific category allows to build an exhaustive coverage of items; and enables serving a long tail of customers looking for niche products/services.

Better and more efficient logistics; owning full category-specific supply chain can help with better SLAs. Some categories like pharmaceuticals, meat etc. require specialized logistics and fulfillment capabilities - doing so as part of a multi-category supply chain is difficult.

Better and more customized workflows; mirroring the way business is done in respective sectors. Also, the value-added services like credit, book-keeping etc can be customized basis the category

Better gross margins through higher volumes (although, each category has different GMs - for eg fruits & vegetables offer thin margins while spices offer high margins)

Going deeper in a category can help build more sticky relationships with buyers and sellers; and provide some defensibility to the business

Within the B2B space, unlike B2C, vertical marketplaces may have an upper hand as compared to horizontals.

…

Thank you for reading! Please share it with people who you think might find it interesting :)

You can also follow me on Twitter here.

Disclaimer: All views expressed in this blog are mine, and do not represent the views of my employer