[#6] Netflix - A business on a treadmill (Developing a bear case)

An attempt to show how Netflix would find it tough to continue on its current growth trajectory

Netflix is a leading provider of subscription video on demand (SVOD) services and has rapidly increased its subscriber base in recent years, both in the US and globally. It would be an understatement to say that Netflix is one of the most popular digital content offerings.

Investors love it too! Here’s how the stock has performed over the past 5 years.

…

In this article, I first take a look at one of the critical factors that enabled Netflix to achieve this position – its content spend. Then, I attempt to build a bear case, on how Netflix might not be able to exhibit the same level of success going ahead as it has demonstrated in the past.

…

Understanding Netflix’s business model and the role of content spend

The rapid growth of Netflix is mainly attributed to Netflix’s flywheel of engagement.

As Netflix spends heavily on content; the better content attracts more subscriptions, and Netflix invests most of the added cash flow to originate better content. It has also incorporated higher personalization in the flywheel, leading to more engagement. More engagement also helps in better content curation and production, adding to the positive feedback loop.

As Nick Johnson, co-author of Modern Monopolies, explains:

The genius of Netflix was in applying a digital distribution model to what is essentially the same linear business model of a TV network. Netflix’s business in fact looks a lot like HBO, but instead of relying on cable subscriptions and telecom relationships, Netflix goes direct to the customer. This strategy has greatly driven down the cost of distribution. The economics of scarcity that have driven TV – one new episode a week, drawn out release schedules and so on – disappear with a digital distribution model.

With Netflix’s model, you’re no longer trying to please advertisers by getting viewers to tune in live. Instead you simply want viewers to stay hooked as long as possible. Goodbye live TV, hello binge watching.

The challenge, of course, is that you need enough content to keep those viewers watching. Which means Netflix always needs a lot of new content – a lot more than the typical TV channel will ever churn out.

The goal for Netflix is that it can get enough consumers hooked, and make enough from subscriptions, to make more money than the cost of serving up a nearly endless well of (hopefully quality) content. That’s Netflix’s business model in a nutshell: building scale on top of fixed costs and hoping that the growth of the former continues to outpace the growth of the latter.

Netflix’s goal is to functionally ‘replace the bundle’ – to have so much diverse content that customers don’t need another general entertainment aggregator, be it Hulu or DirecTV Now. Audiences would still have a few focused carve outs, such as HBO, ESPN or Disney, but rather than enlisting for Discovery + AMC + ABC + Nickelodeon + Showtime etc., the average household would just need Netflix.

Here’s a breakup of the content spend that Netflix has incurred over the years:

One of the key shifts that has happened over the past few years has been Netflix’s increasing investment in own content. While initially focusing on acting as a distributor of content providers like Disney, Comcast etc, it understood the importance of producing its own content. The company realized that if online streaming is the future, it would only be a matter of time until other media companies entered the field themselves instead of licensing their movies and TV shows to Netflix. So with a library of original content, Netflix was preparing for eventualities such as Disney removing its content from Netflix to stream on its own platform.

Accordingly, Netflix is now focused on investing in content that it can own exclusively and in perpetuity, rather than renting it.

In 2019, Netflix spent around $15B in content, about 60% of which will stay on the service indefinitely as they are owned, self-produced originals. On an overall content library basis, close to 40% of the content is now estimated to be owned by Netflix.

…

Netflix’s bear case

Netflix is playing a long game just like most successful platform businesses; and is spending heavily on content today with the goal of three things happening:

Its subscribers would rise at a rapid clip

It would be able to raise its prices

Eventually, it would be able to reduce its spend on content and start gaining from operating leverage

However, here are some reasons I believe Netflix may not be able to achieve these targets, atleast not very easily.

Reason 1: Saturation in core market – USA

USA has, since the beginning, been the biggest market for Netflix. The company has ~70 million subscribers in USA, which as of 2017 had 126 million households. However, given the widespread account sharing, it can be reasonably inferred that Netflix’s penetration in USA is well above 50%.

While additional market share is definitely there to be captured, but it is going to get incrementally tougher to reach new households.

Reason 2: Customers may not be as price inelastic as previously assumed

Till recently, Netflix has competed mainly with linear TV bundles at one-fifth the price, and hence offered a compelling value proposition.

Now, Netflix operates in a crowded space where it is one of the most expensive options. Going forward, it must compete with ‘free’ as Apple and Amazon bundle their SVOD services into their core products and Disney+ pricing is almost half that of Netflix’s.

For the same $12.99 monthly price as Netflix, consumers can get a bundle of Hulu, Disney+, and ESPN+. For $10/month, they can get Prime Video – along with all the other perks of Prime membership

In January 2019, Netflix raised its prices marginally in some regions (increases ranging from USD 1 – 2 per month depending on the plans). In the following quarter, Netflix lost 123,000 U.S. subscribers. The company's international subscriber count also failed to reach Netflix's forecasts, going up by only 2.8 million, as opposed to the projected 5 million.

This is what Netflix said in its shareholder letter:

Our missed forecast was across all regions, but slightly more so in regions with price increases.

Price elasticity of Netflix subscribers is a function of pricing by competitors; and while there might be headroom to increase prices further, it may come at the cost of sacrificing subscriber growth.

Reason 3: Growth from international markets comes with its own share of troubles

With US market showing signs of saturation, Netflix has been pursuing growth in other markets.

However, Netflix will face competition on two main fronts — content and price — that will make it really difficult to grow its subscribers in a cost effective manner. For non-English speaking countries, Netflix would have to spend a lot of money to develop / license local language content. A good example is India, where Netflix is working hard to compete with Hotstar (which currently has a vastly superior local-language content library).

Secondly, pricing in emerging markets (from which Netflix expects the bulk of its growth to come from) would be a constraint. Netflix’s Average Revenue per User (ARPU) is most countries is lower than in USA, and in large markets like India, Netflix has also launched mobile-only plans to get more subscribers, which drastically reduce the ARPU. Moreover, these customers may be even more price-sensitive than their US counterparts, effectively putting a cap on price increases possible.

Again, taking the example of India, Netflix in India costs about twice as much as the average cable TV package, which would narrow Netflix's addressable market considerably. As per Evercore Research, an equity advisory firm in USA:

While Netflix may certainly appeal to upper-income Indian households, we think that the company will be hard pressed to penetrate more than 5% of the population in the foreseeable future.

Reason 4: Return from content spend may not stay high enough

Earlier, we spoke about how Netflix wants to build a content library that it can own in perpetuity, essentially incurring a fixed cost now and benefit from it over several years / decades.

However, content has an expiry date.

For every series like ‘Friends’ or ‘The Office’ which have stayed at top of viewing lists for several years (both of which are not owned by Netflix, by the away), there are several hundred shows which are not seen or remembered beyond a year or two post their release. Industry estimate suggest that the average ‘shelf life’ of original content would be 3-4 years, and hence, it seems that the ‘perpetual content ownership’ argument breaks down.

Now, in such a situation, content spend needs to be analysed from two angles: how much more user engagement does it drive, and for how long does it drive the engagement.

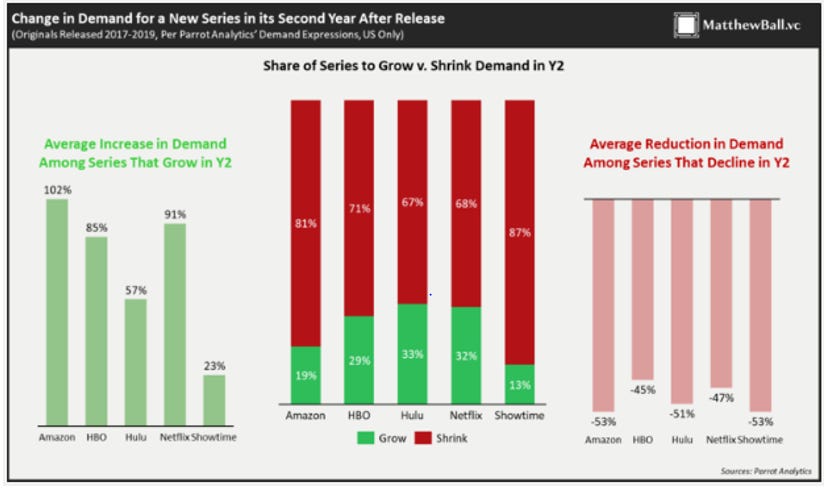

Here are a few interesting charts posted by Matthew Ball, former global Head of Strategy for Amazon Studios. (Note that the data pertains to the US market only)

First, looking at 2019 data, HBO’s new series were, on an average, twice as in-demand as those of Netflix and Amazon. This, of course, translates into a huge differential in ‘user engagement per unit of content’, the metric by which we can measure the efficiency of content spend.

Secondly, we now need to look at duration for which Netflix is able to drive engagement through its content. It seems that Netflix’s original shows (1) are the most likely to grow year-over-year; (2) will see the greatest growth when they grow; (3) and when they decline, they will tend to decline the least.

However, as Matthew suggests, Netflix’s series were, on an average, the least demanded to begin with (as depicted stated in first chart). As such, they need far greater growth to meet the performance of competing services, and the same rate of growth doesn’t mean the same overall growth.

A good way to think about this is through college GPAs: the difference between a 3.3 and 3.4 is much less significant and easier than moving from a 3.8 to a 3.9. On balance, Netflix has weak grades. Semester-to-semester improvements help, but the average remains low.

Now, finally, let’s take a look at not just how Netflix’s shows performed on average, but how many ‘above average’ shows Netflix managed to release. According to Parrot Analytics, Netflix released 16 ‘Outstanding or Better’ seasons of TV in 2019 (this means ‘Demand Expressions’ were >8x that of the average series, equivalent to the top 2.5% of all releases). This was more than any other video service. However, this is largely a result of Netflix’s enormous output. Only 12% of Netflix’s 135 total releases in 2019 qualified as “Outstanding or Better”, while 55% (or 74) were average or below.

Overall, HBO’s 2019 series were more than 7x more in-demand than those of the average TV network (including History, ABC, Fox, History, etc.), or 12x when including Game of Thrones. This compares to 4.0x for Apple TV+ and Netflix, 5.6 for Amazon, Showtime, and Hulu, 5.8 for CBS, and 6.8 for Starz.

Effectively, Netflix is ahead mainly because it is spending way more than competitors. Hence, the return per unit of content remains low, for now.

…

A business on a treadmill

In Lewis Carroll’s book ‘Through the Looking Glass’, there is a scene where Alice and the Red Queen are running constantly but still remain in the same spot. The Queen says to a perplexed Alice – “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

I feel Netflix’s business model is akin to running on a treadmill: Netflix constantly needs more subscribers, it constantly needs to generate more content, it also constantly needs to make sure that its content is on an aggregate, more in-demand than its competitors.

Failing to do one of them means failing to do any of them.

(Views are personal and do not, in any way, represent the views of my employer)

...

Some interesting reads

1. Swiggy It! (Rohit Manchanda)

Rohit does a deep dive into the unit economics of Swiggy. He looks at what’s working, what’s not. Excellent, data-driven exercise.

2. On Josh Wolfe - Authentic contrarians vs consensus contrarians (Leon Lin)

Josh Wolfe is the co-founder of Lux Capital, a venture capital firm and as many would agree, one of the smartest people in the investing ecosystem. This article does a good job of explaining his thought process.

References:

(1) https://www.applicoinc.com/blog/netflixs-defensibility-problem-not-tech-companies/

(2)https://www.matthewball.vc/all/contentcarscomparisons

Thank you for reading! Please share it with people whom you think might find it interesting :)

And if you wish to receive such posts directly in your inbox, please subscribe. No spam, ever!

You can also follow me on Twitter here.