[#13] Counter-positioning as a business strategy

Finding part of the incumbent's business model that they can't (or wouldn't want to) do without

Hey! Welcome to Marginal Futility. This blog is my attempt to summarize and share some interesting things I come across, especially related to business, finance and tech. I have previously written about the power law in venture capital, business lessons from Amazon and common errors in estimating market size. You can find the full archive here.

You can subscribe below if you wish to receive updates directly in your mailbox. No spam, ever! :)

(Disclaimer: All views expressed in this blog are mine; and do not, in any way, represent the views of my employer.)

On to today’s article…

“How will you face the incumbent?”

This question (or a variation of it) often appears in conversations around startups / new entrants. In most cases, it is a legitimate question - even if a startup finds an excellent business model, there is a high possibility of an incumbent copying / improving upon it; and end up out-competing the new entrant(s).

But, there are enough number of cases where startups / new entrants have managed to compete with powerful, seemingly unassailable, behemoths. The incumbents eventually try to fight back, but often too late. Think Netflix vs Blockbuster, Vanguard vs Fidelity, Apple vs Nokia, Zerodha vs large brokerages etc. While popular commentary often attributes this to lack of vision / poor management / inertia etc on part of the incumbents, that certainly cannot be a reasonable explanation in several cases; especially considering the fact that we are talking about large, successful incumbents.

…

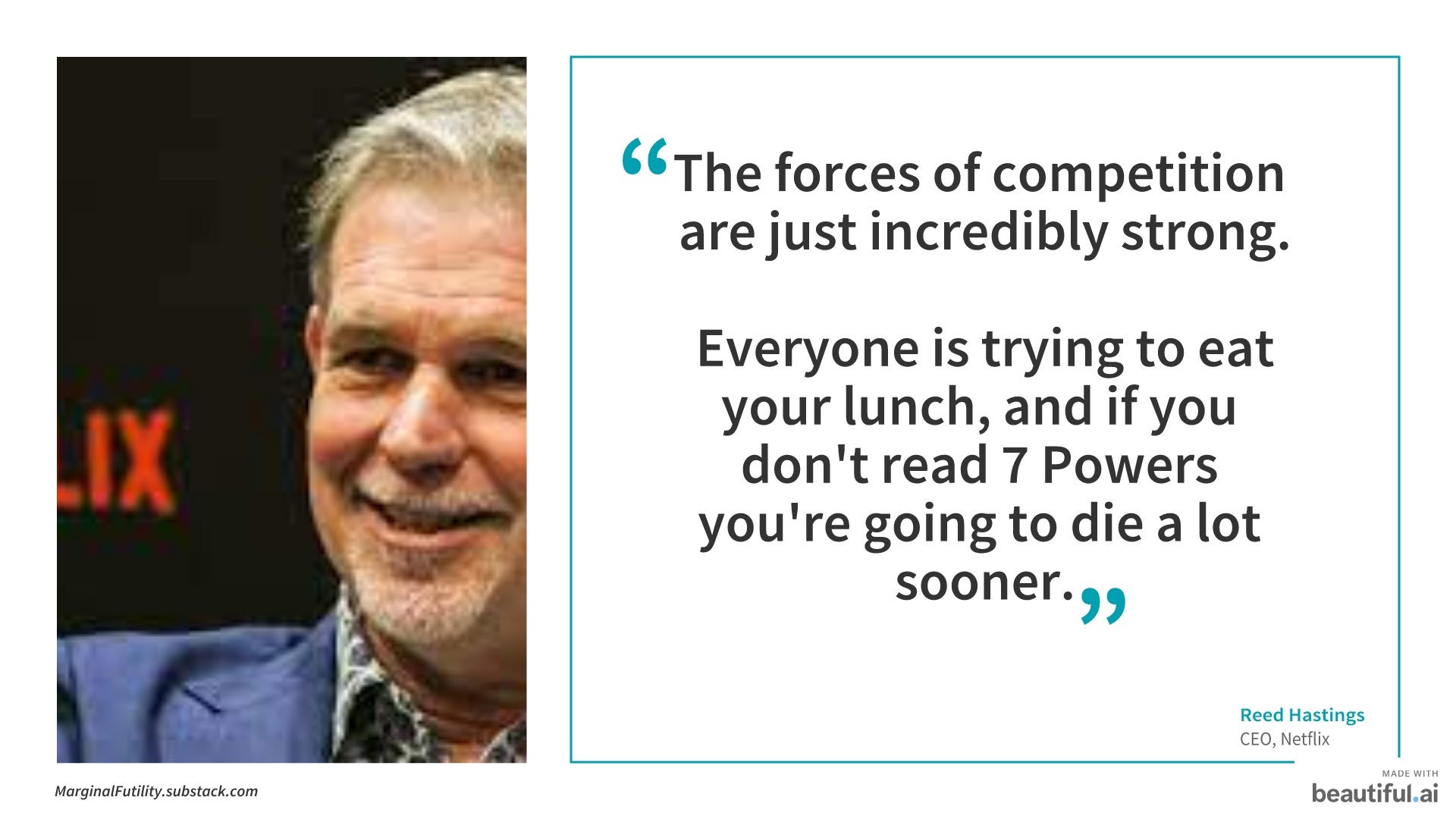

I recently read the book ‘7 Powers: The Foundations of Business Strategy’ by Hamilton Helmer. It is an excellent primer on business strategy; and very well attuned to the current business landscape. Mr. Helmer published this book in 2016; after a career of working with over 200 clients as a strategy consultant, including Netflix, Spotify, and Adobe.

Here’s what Reed Hastings, CEO of Netflix, says about this book:

This book defines the goal of strategy as creating a way to generate “persistent differential returns” for a business. In order to accomplish this, a successful strategy needs to have two components: a ‘benefit’ and a ‘barrier’.

The ‘benefit’ refers to the conditions that lead to cash flow augmentation / market share gains etc (the ‘differential returns’ aspect of the definition). But perhaps, the more important part of the strategy is establishing the ‘barrier’, which prevents existing and potential competitors from arbitraging away the benefit (the ‘persistent returns’ aspect of the definition). Together, these two elements help build the ‘economic moat’ of a business.

Hamilton outlines 7 Powers (strategies) that can help accomplish these goals.

I found “Counter Positioning” the most interesting, and it helps answer the question we saw earlier.

…

Counter-positioning defined

A newcomer adopts a new, superior business model which the incumbent does NOT mimic due to anticipated damage to their existing business.

Put simply, the challenger firm adopts a business model that is “counter-positioned” to the incumbent. Adopting the new business model would end up harming the incumbent’s existing business.

At this point, think from the perspective of the incumbent which is battling with two questions:

Should we continue with the current business model, risking losing market share to the new entrant?

Or, should we adopt the new (possibly unproven) business model risking our existing business?

It is very easy to say that if the new business model is “better” the second approach should be followed, but change is hard. It requires tons of resources and alignment. Add to it the clear risk of damaging / cannibalizing the existing line of business. All these factors result in the incumbent either delaying the decision to adopt the new business model, or doing so in a limited manner.

…

Examples of Counter positioning

Netflix vs Blockbuster

Blockbuster was in the business of video / movie rentals through brick and mortar stores. At its peak, Blockbuster had 9,000 stores.

When Netflix launched its business in 1997, it adopted a counter-positioned business model to that of Blockbuster: DVD by mail (instead of in-stores) and no late fees unlike Blockbuster.

Both of these aspects obviously sound better from the viewpoint of customers. However, Blockbuster did not imitate Netflix - even though it could have easily done so. Why? Because it would have hurt their existing business significantly. Late fees constituted a significant portion of Blockbuster’s revenues - In 2000, Blockbuster said it made $800 million in late fees, or 16% of its revenue. Further, one of Blockbuster’s core value propositions was the superior in-store experience. Launching a DVD by mail service would be counter to one of their key selling points. Further, the stores were also a source of another highly profitable and significant revenue stream for Blockbuster - concessions (like popcorn, candies etc). All in all, the NPV of starting a DVD by mail service and eliminating late fees would have been highly negative for Blockbuster for a significant period of time - and hence Blockbuster did nothing.

While it is easy to say that Blockbuster should have taken a really long term view to this, the fact remains that not all companies have the ability or willingness to self-disrupt themselves and think in terms of decades, rather than years.

There are several other examples of this phenomenon:

Vanguard taking on active mutual funds like Fidelity by offering passive mutual funds. The incumbents were too late to add passive funds to their list of offerings because of the significantly lower fees on them and the risk of cannibalizing their highly lucrative active mutual funds

Robinhood (and other discount brokerages) taking on erstwhile bigger brokerages by offering trades for zero commission and instead relying on payment for order flow. The incumbents could not (or rather, did not) compete because of the significant revenues they derived from their brokerage commissions and research services

Public.com taking on Robinhood by relying on optional tips from users for executing their trades instead of payment for order flow, which is how Robinhood makes bulk of its revenues

Netflix offering online streaming services while players like HBO not jumping into it (until quite later) because of the highly profitable contracts that they had with cable providers and the significant revenues from cable subscriptions (Note that HBO’s parent company was Time Warner - one of the largest cable providers in USA)

Dell going the direct-to-consumer route while incumbents like Compaq not following it because of the fear of hurting their well-established distribution network (with channel partners)

Lambda School charging no upfront fees for software engineering courses and instead relying on Income Sharing Agreements, while incumbents (traditional engineering colleges) not following suite because of the reliance on fees to support their cost structures and the focus on longer duration programs

…

Closing Thoughts

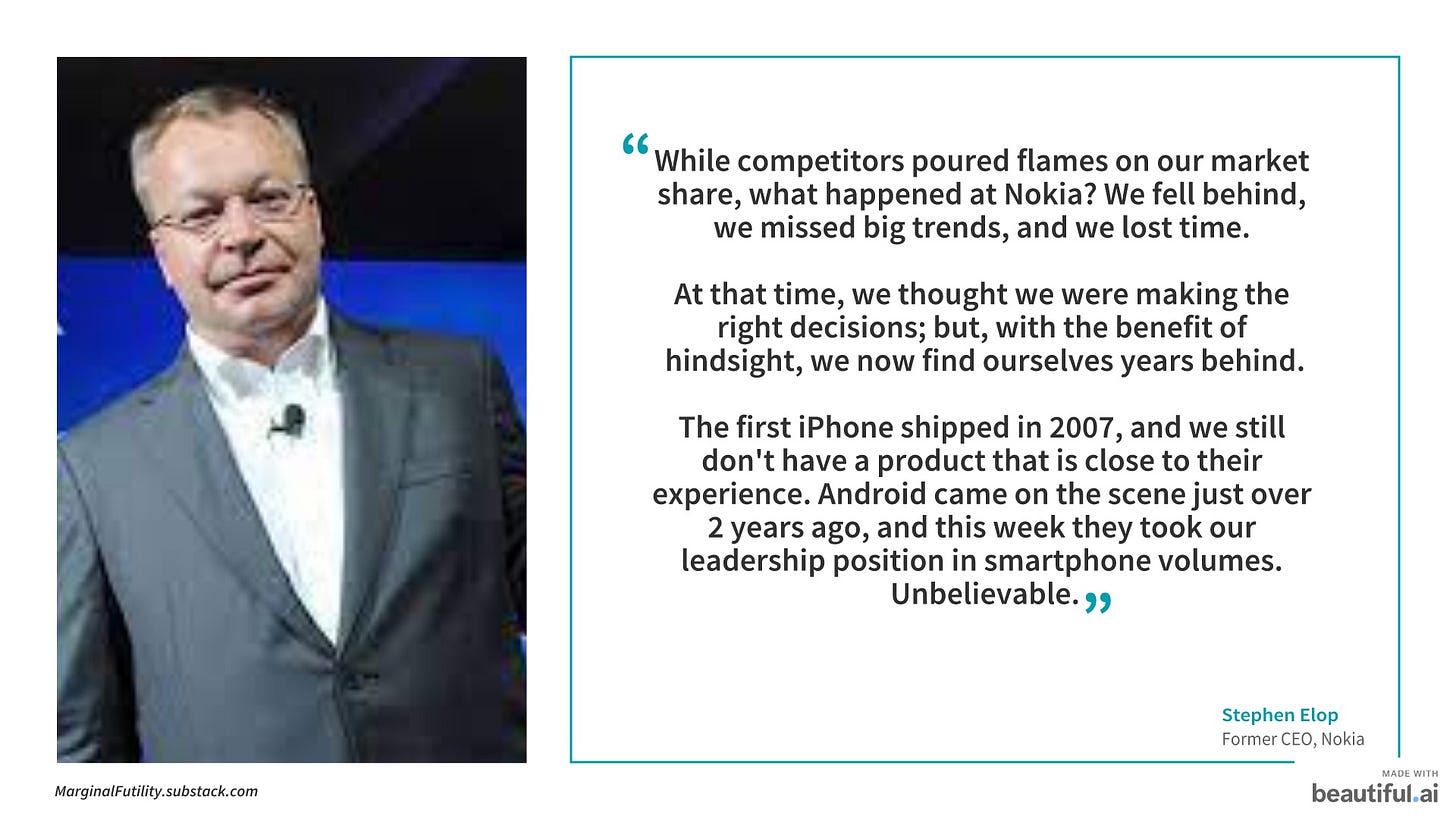

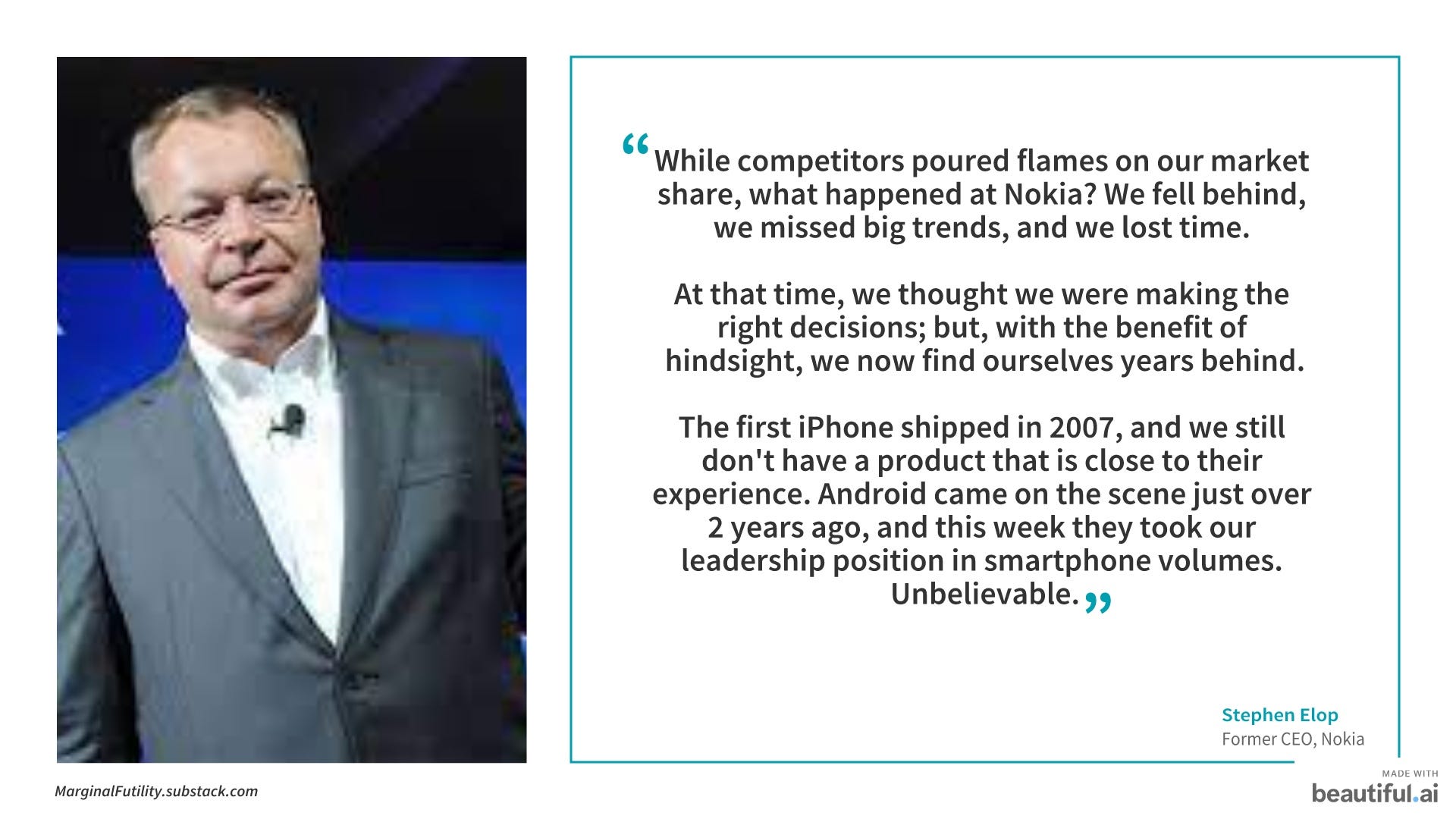

Counter-positioning, while difficult to find an execute, is one of the toughest and incredibly frustrating business challenges an incumbent can face. Have a look at this excerpt from the ’Burning Platform’ memo by Nokia’s former CEO, Stephen Elop, written in 2014:

Counter-positioning applies only relative to the incumbent(s) and does not say anything with respect to other firms opting for the new business model - hence, it is only a ‘partial strategy’

Interesting things I read this week

1. Opportunities in Education (Erik Torenberg)

When I look at the state of education, I can't help but feel like something needs to be done. I already talked about how higher education is a bubble, but this week I wanted to dive into where I see opportunities for investment & innovation, and how we can think about building education institutions in the future.

2. Power to the Person (Packy McCormick)

The Creator Economy and NFTs are massive human potential unlocks. Even if certain assets are in a short-term bubble, we are on an inexorable march towards individuals mattering more than institutions.

We’re on the precipice of a creative explosion, fueled by putting power, and the ability to generate wealth, in the hands of the people. Armed with powerful technical and financial tools, individuals will be able to launch and scale increasingly complex projects and businesses

Thank you for reading! Please share it with people who you think might find it interesting :)

You can also follow me on Twitter here.

(Disclaimer: All views expressed in this blog are mine; and do not, in any way, represent the views of my employer.)